The Weis Wave indicator for Tradesignal combines volume and trend information to detect turning points of the market.

Author: Kahler Philipp

Tradesignal Implied Volatility and IV Percentile Scanner

Use free data from the web and load it into Tradesignal to scan for implied volatility and IV percentile. Full code given for free

IV Percentile – when to sell volatility

IV percentile and IV rank both describe implied volatility. Which one is better in finding out if it is time to sell volatility? Read the answer in this article

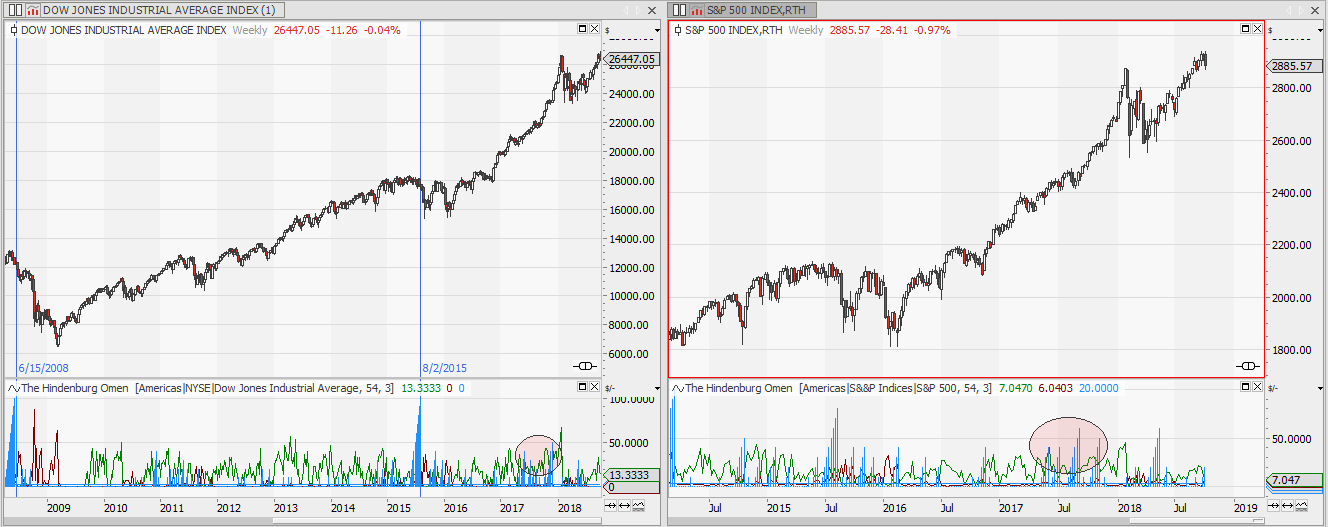

The Hindenburg Omen – Stock Market Crash Ahead?

The Hindenburg Omen is a market breadth indicator analyzing new highs and lows on the market. It signals the end of the current bull market. Tradesignal Indicator Code is provided

Implied vs. Realized Volatility for NASDAQ100 stocks

Comparing implied volatility to realized volatility can show you the right stocks to sell volatility. An overview over the implied and long term realized volatility of NADAQ100 stocks is given.

Distribution of Returns

“Tomorrow never happens. It’s all the same fucking day, man. ” Janis Joplin

Bet on Bollinger

Ever since John Bollinger introduced his Bollinger Bands in the early 1980s the bands have been a favourite indicator to all technical trades. This article is about the prediction capabilities of Bollinger bands.

Scanning for Support and Resistance Probabilities

Scanning a market for support and resistance levels which will most likely not be penetrated in the near future is key for strategies like short options or vertical spreads. This article hows how RSI can be used to solve this problem.

Weekend Reading Recommendation

The markets will go up and down, and usually it’s not my business why they do it, I am just interested in making my luck with a position on the right side of the trade.

Backtesting Market Volatility

Backtesting if historical volatility or Kahler’s volatility gives a better prognosis for future volatility. Calculating the average prediction error of these two volatility indicators. Testing for the influence of data points used on the quality of the prediction. Comparing the findings to implied volatility to generate a trade idea.

Demystifying the 200 day average

The 200 day moving average is a classic of technical analysis. but is there any edge or statistical significance in it? How do equity and Forex market differ when it comes to this indicator? See the analysis and the answer to these questions.

Google EOD csv stock price data download

Sometimes my data provider has not got the data I am looking for. Searching for downloadable csv data I recently came across google spreadsheets. It provides an easy way to get historical stock price data. Save it as csv and use it with your Tradesignal.

Money for nothing

We already had a post regarding the mean reverting tendency of Volatility, now it`s time to make some money using this information.

Seasonal trouble ahead

Seasonal Projection and Volatility prognosis for german DAX. Trouble ahead…

KVOL Volatility part 2

How to calculate volatility based on the expected return of a straddle strategy has been shown in part 1 of fair bet volatility KVOL. Using and Displaying K-Volatility: KVOL uses the given amount of historic returns to calculate an expected value of an at the money put and call option. The sum of these prices are… Continue reading KVOL Volatility part 2

Statistics of VIX

This article is about the statistics of VIX. What determines if it is better to sell or to buy volatility. Some simple statistics can provide the answer and also show the dangers of this kind of volatility trade.

Kahler’s fair bet volatility

Volatility is a measure of risk. It describes how far a commodity will most probably move within a given period of time. The most common measure for volatility is historical volatility. But I do not like the complicated formula for standard deviation. There has to be a better way to explain and calculate volatility…. Implied… Continue reading Kahler’s fair bet volatility

A graphical approach to indicator testing

Scatter charts are a great tool to test the prognosis quality of your indicators. A visual approach on indicator quality can help you to get rid of curve fitting when using classical or machine learning trading strategies.

Machine learning: kNN algorithm explained

Can inspiration be replaced by brute force? This article shows how to program and possibly use a simple kNN algorithm to trade Brent. A two dimensional data set will be used. RSI will determine if tomorrows market will move up or down.

Using Autocorrelation for phase detection

Autocorrelation is the correlation of the market with a delayed copy of itself. Usually calculated for a one day time-shift, it is a valuable indicator of the trendiness of the market. If today is up and tomorrow is also up this would constitute a positive autocorrelation. If tomorrows market move is always in the opposite… Continue reading Using Autocorrelation for phase detection